Table of Contents

- Introduction to Gold Investment Pyramid: Don’t Ask “What,” Ask “Why” First

- Level 1: Wealth Insurance (The Most Critical Foundation)

- Level 2: Savings & Investment (Building Wealth Systematically)

- Levels 3 & 4: Active Investing & Speculation (For the More Advanced)

- Conclusion: Build Your Pyramid According to the Right Objectives

Introduction to Gold Investment Pyramid: Don’t Ask “What,” Ask “Why” First

Many people who are enthusiastic about starting their journey with gold often make the same initial mistake. They immediately jump to the question, “which product is the best one to buy?” or “which company should I choose?”. This is a significant error that can lead to losses or disappointment down the line. Imagine you want to build a house. Would you go straight to the hardware shop and start buying bricks and cement at random? Of course not. You would start with a blueprint, a clear plan of action first.

It’s exactly the same with investing in gold. Before you choose the ‘bricks’ (the product), you must have a ‘blueprint’ (a strategy). You must ask a far more important question: “What exactly is my objective for investing in gold?”. Are you looking to protect your wealth? Accumulate a retirement fund? Or generate quick profits? Your answer to this question will determine everything that follows. To help you, let’s use the ‘Gold Investment Pyramid‘ model—a clear framework to structure your strategy from the safest level to the riskiest.

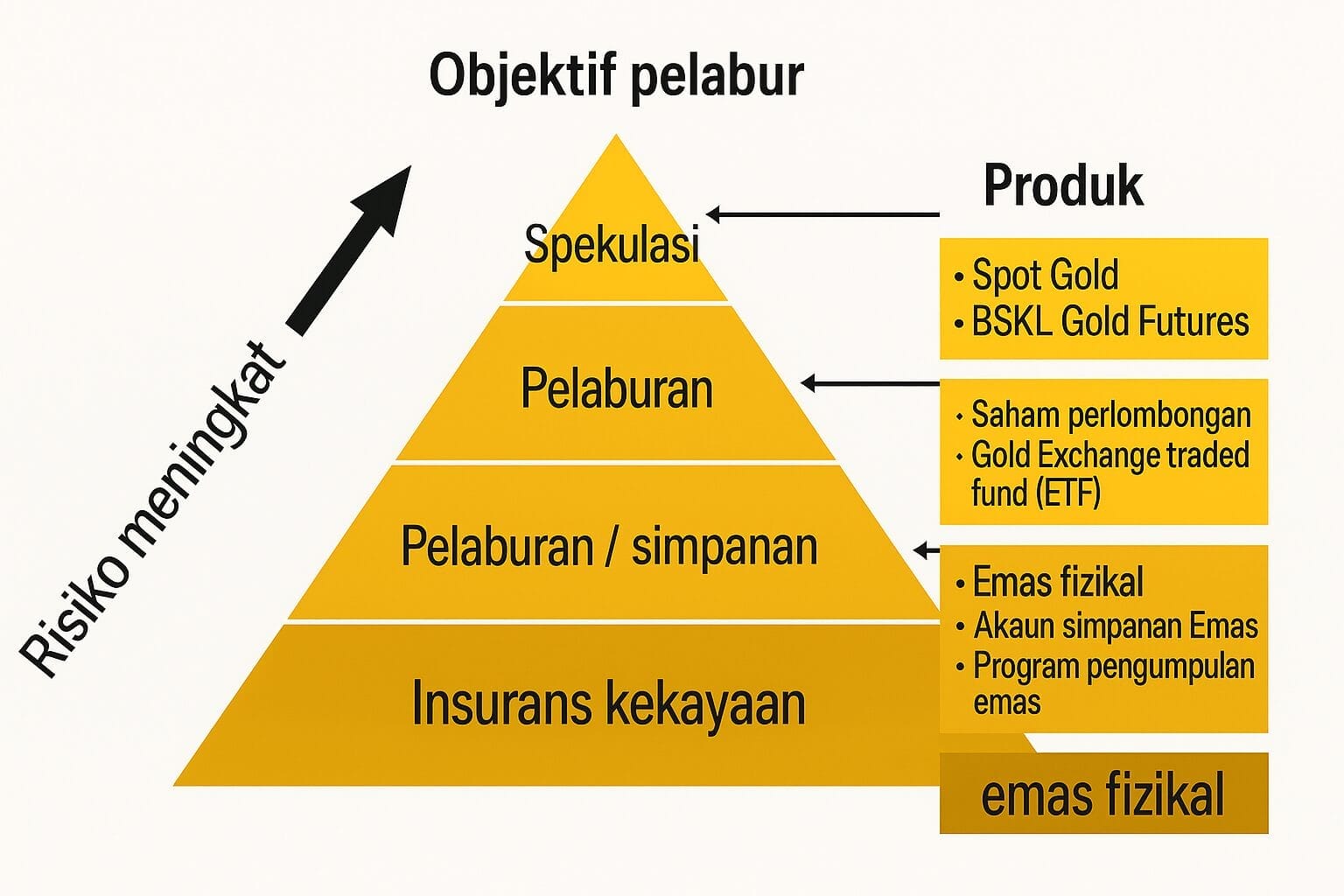

Level 1: Wealth Insurance (The Most Critical Foundation of the Gold Investment Pyramid)

This is the base or foundation of the pyramid. It’s the widest, most solid, and most important level that everyone should have, regardless of whether you are a new or seasoned investor. The objective at this level is not about getting rich, but about ensuring you don’t become poor. It serves as your financial fortress against unseen economic threats like inflation and currency devaluation. The primary goal within this foundational stage of the Gold Investment Pyramid is absolute protection.

1. The Objective: To Protect Your Purchasing Power from the ‘Silent Thief’ of Inflation

Think of this first level of the Gold Investment Pyramid as buying an “insurance policy” for your money. When you buy car insurance, you don’t hope to have an accident. You buy it to protect yourself just in case something bad happens. It’s the same with gold at this level. Your main objective is to protect your existing wealth from being eroded by the ‘silent thief’ known as inflation. Every year, the value of the paper money in your bank account decreases. Gold tends to act in the opposite way. When the price of goods rises, the value of your gold savings will also rise, ensuring your purchasing power is preserved.

The benefit of this is immense in terms of peace of mind. You can sleep soundly at night knowing that a portion of your savings is safe from currency devaluation, political instability, or a financial crisis. This objective is about building a solid ’emergency fund’ that holds its value, unaffected by government policies or stock market volatility. It’s the most responsible first step in any financial plan. This is the true essence of the Gold Investment Pyramid.

2. The Product of Choice: Physical Gold (Bars & Coins) That You Hold Yourself

For the purpose of protection and insurance, nothing beats holding the asset physically in your own hands. Gold bars and coins (such as Sovereigns or Britannias) are the best choice to meet the objective at this level of the Gold Investment Pyramid. Why? Because they have zero ‘counterparty risk’. Their value does not depend on the promise or stability of any company, bank, or financial institution. They are entirely your asset. As long as you hold them, they are yours.

The benefit is that you have 100% control over your asset. It cannot be frozen, it cannot be deleted from a system, and its value is recognised all over the world, no matter what happens to the banking system or stock markets. Holding physical gold is the purest and safest way to store wealth. It is the concrete foundation of your personal Gold Investment Pyramid, a base that will support all your other investment levels. This is the most fundamental objective and should never be overlooked.

Level 2: Savings & Investment (Building Wealth Systematically)

Only after you have successfully built a solid foundation of protection within your Gold Investment Pyramid can you move on to the next level with confidence. Our objective here begins to shift from merely defending wealth to systematically building it for long-term goals. If Level 1 is your shield, Level 2 is your action plan to accumulate ‘treasure’ step by step. This level is all about stable, disciplined growth. The objective for this part of the Gold Investment Pyramid is to build a meaningful future fund.

1. The Objective: To Accumulate an Asset for Future Goals

At the second level of the Gold Investment Pyramid, you purchase gold periodically (for example, every month) for specific future purposes. Your goal might be to build an education fund for your children, accumulate a comfortable retirement pot, save for a deposit on your first home, or fund a once-in-a-lifetime trip. Here, you are not only preserving value as in Level 1, but you are also actively expecting capital growth over the medium to long term (5 to 20 years).

The main benefit of this strategy is that it instils a very high level of financial discipline. It forces you to save in a real asset whose value tends to increase, rather than just saving paper money whose value is guaranteed to decrease. Every gram you accumulate is a step forward towards achieving your dreams. A clear objective like this will keep you more committed and focused on your financial journey. It transforms your saving habit from a passive act to a proactive one of building real wealth.

2. The Product of Choice: Physical Gold or a Gold Accumulation Account

How can you achieve this objective within your Gold Investment Pyramid? In addition to continuing to add to your physical gold holdings (perhaps buying a 1-gram bar or a small coin each month), you can also use modern, flexible products like a Gold Accumulation Programme (GAP). An account like this allows you to buy gold with a very small amount of capital, as little as RM 100, at any time through a mobile app. It makes consistent saving incredibly accessible.

The benefits are huge, especially for those just starting out. You don’t need to save up a large sum of money to buy a bigger bar. You can save according to your own budget, consistently. These accounts are also typically 100% backed by physical gold, which means every Ringgit you put in is converted into a real weight of gold that is securely stored for you. They are flexible, easily accessible, and secure. This makes the objective of building wealth through the Gold Investment Pyramid achievable for people from all walks of life, not just the wealthy elite.

Levels 3 & 4: Active Investing & Speculation (For the More Advanced)

The top two levels of the Gold Investment Pyramid are for those with a higher risk appetite, a deep understanding of the markets, and the time to actively monitor their investments. We are now moving from the ‘saver’ zone into the ‘investor’ and ‘trader’ zones. The objective here is no longer just to protect or save, but to actively generate profits from market movements in a shorter time frame. This is the pointy, less stable peak of the pyramid, and it is certainly not for everyone. This part of the Gold Investment Pyramid demands expertise.

1. Level 3 (Active Investing): Seeking Profits Like in the Stock Market

At the third level of the Gold Investment Pyramid, you start to view gold as an asset class for generating returns, much like you would view stocks or unit trusts. Your objective is to buy low and sell high to make a capital gain. You might invest in gold-backed derivative products such as Exchange-Traded Funds (Gold ETFs) or shares in gold mining companies. These products are traded on the stock exchange, making them very easy to buy and sell on a daily basis.

The benefit is that they have the potential to deliver higher and faster returns compared to simply holding physical gold. However, this comes with a much greater market risk. The value of ETFs and mining stocks can fall sharply due to market sentiment, company performance, or global economic factors. Most importantly, you must remember that with these products, you do not own any actual physical gold. You simply own a ‘paper’ representation of gold’s value.

2. Level 4 (Speculation): High-Risk, Short-Term Gains

This is the very pinnacle of the Gold Investment Pyramid, the smallest and riskiest level. It is reserved for professional traders who attempt to make profits from the fluctuations in the gold price over very short periods, perhaps within days, hours, or even minutes. The objective here is pure speculation. The instruments often used at this level include Gold Futures or Contracts for Difference (CFDs). This is the most advanced objective in the Gold Investment Pyramid.

These instruments use ‘leverage’, which means you can control a large value of gold with only a small amount of capital. The benefit is the potential for huge and rapid profits if your prediction is correct. However, the risk is equally immense. If the market moves against you, you can lose your entire capital very quickly, and sometimes even more than your initial investment. This is an objective that should only be pursued by experts who are fully prepared to accept significant losses.

Conclusion: Build Your Pyramid According to the Right Objectives

Understanding your objectives using the Gold Investment Pyramid model is the most critical first step in your journey. It gives you a clear roadmap and prevents you from making major mistakes, such as using a speculative product (Level 4) for long-term savings (Level 2). Each level of the Gold Investment Pyramid has its own purpose and its own tools, and mixing them up is a recipe for failure. The Gold Investment Pyramid framework logically structures your strategy.

The most important piece of advice is this: always start from the bottom of the pyramid. Never jump straight to the top. Build your “Wealth Insurance” foundation with physical gold first. Ensure a portion of your wealth is truly safe and secure. After that, you can begin building your “Savings & Investment” level. Only when these two lower levels are solid should you even consider putting a small part of your portfolio into the riskier upper levels. By identifying your objectives first, you can then choose the right products and build a truly robust and suitable gold portfolio for your future.

✨ WANT TO START SAVING IN GOLD?

With just RM100, you can begin your gold savings journey with Public Gold.

This is the perfect opportunity to build a stronger and more secure financial future.